Credit refers to an agreement to pay or be paid in the future. Your personal credit score measures how trustworthy credit bureaus think you are to repay the money you owe. Similarly, your business credit score measures how reliable credit bureaus think your business is to repay the money it owes. These credit bureaus base their calculations on several factors, which I will detail later. For now, let us discuss why strong credit scores are important, how to establish a strong personal and business credit score, and how to check your credit scores.

The Importance of Strong Credit Scores

As I mentioned in the introduction, credit scores indicate your trustworthiness to repay the money you owe. Since it is an objective, independent measure based on relevant details about your credit transactions, it is widely used among banks, suppliers, potential investors and partners, and insurance agencies. Improving your credit score is one of the best ways to improve your chances of getting loans approved, reducing your insurance rates, lowering interest rates, extending credit terms with suppliers, and attracting quality business partners. Therefore, it is an important factor to consider as you plan your business.

How to Establish Personal and Business Credit Scores

Personal credit scores

The most common way to begin building a personal credit score is to obtain a traditional credit card from a bank (Bank of America, Capital One, Chase, American Express, etc.), or a retail store credit card from a gas station, discount store, or department store (Target, Kohl’s, Belk, American Eagle, etc.). Do careful research on which best suits your needs. Now, when you spend money on credit cards, you are effectively spending money that is not yours. As a result, you are creating short-term debt for yourself. Many people do not take this seriously and fall into crippling credit card debt. Credit cards have extraordinarily high interest rates (up to 30%), so always try repaying your credit card balances before they are due, if possible. At the very least, make the minimum monthly payments. However, please understand that if you make the minimum monthly payments, your balance will roll over to the next month, and you will incur that steep interest on the balance that rolls over. It is always ideal to fully pay off your credit card balance. Meeting with a credit specialist at your local bank to discuss the details of your new credit card is a great way to ensure that you avoid common credit card pit falls.

In-Depth Example of Minimum and Full Payments

Let’s suppose you apply for a 30% APR (annual percentage rate) credit card at Capital One and it is issued to you on July 1. Note that APRs can vary between months, even on the same credit card. Suppose the bank allows you to spend up to $1,000 each month on your card. This is called a credit limit, and it will be communicated to you when you receive the card. Each month is known as a “billing cycle.” Your first billing cycle will be from July 1 to August 1. Suppose you spend $500 between July 1 and August 1 and make a $100 payment towards your balance during this period. On the closing date (August 1), your outstanding balance will be the money you incurred on the card ($500) minus the payment you made ($100), resulting in a balance of $400.

Typically, the due date is one month after the closing date, so you will owe $400 on your Capital One card on September 1. Let’s assume you make the minimum payment of $20. Your outstanding balance on September 1 will be reduced to $380 ($400 – $20).

For most credit cards, interest will be charged daily. This means that for every day after September 1 that you maintain an overdue balance, you will incur interest associated with the overdue balance, based on the APR of your credit card at that time, divided by 365. Unpaid interest is added to the overdue balance daily, and interest accrues based on this new amount the next day. This is called compounding, and it is a primary reason why credit card debt can become very unmanageable within a short period of time. Many banks offer an interest-free introductory period (“grace period”) to help you adjust to making on-time payments, but missing these payments could still affect your credit score, as banks report overdue statements to credit bureaus (even though you may not have accrued interest).

In contrast, if you pay off the full $400 by September 1, you avoid any interest charges, and your balance will reset to zero. This is ideal. Then, you avoid the dangerous cycle of compounding interest, which is when interest is charged not only on the original balance but also on any accrued interest from previous months/days. This can cause your debt to grow exponentially over time, especially if you continue to carry a balance from month to month without paying it off in full. As a result, even a small balance can become much harder to manage and repay, leading to higher total interest payments and potentially damaging your credit score. To avoid this, it’s crucial to pay off your full balance each month, if possible, to prevent interest from piling up and keep your credit in good standing.

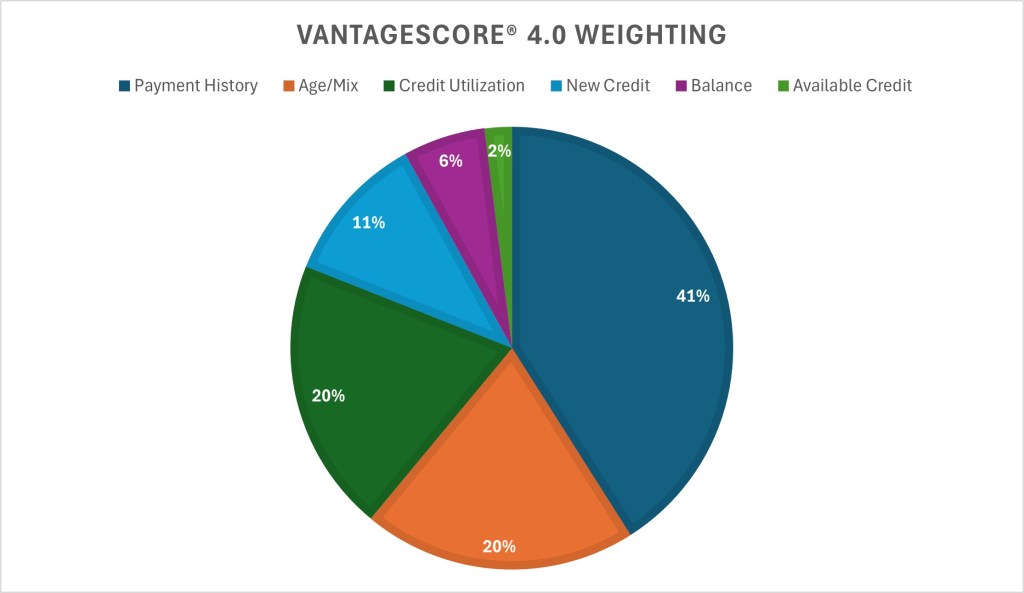

Now that you understand the basics, let’s consider the factors affecting your credit score and how they are weighted. The two main credit scores are FICO® and VantageScore®, which are similar but weigh categories slightly differently. For all practical purposes, the specific differences between the models and each version of the models are not worth discussing, but feel free to research further yourself! These weightings are based on the VantageScore® 4.0, which was jointly created by the three nationwide credit bureaus: Equifax, Experian, and TransUnion.

Note that this is based on a sample study by VantageScore®, and percentages vary based on your credit file, while FICO® has fixed percentages that remain consistent.

1. Payment History (41%):

This is the most important factor in your credit score, accounting for nearly half of the total calculation. Payment history reflects whether you’ve made your credit payments on time, including credit cards, mortgages, auto loans, and so forth. Late payments, collections, and bankruptcies will significantly impact your score, while a clean payment history will help improve it. Even one missed payment may significantly decrease your score, so consistency is absolutely key. Consider enabling automatic payments or setting up reminders to achieve this consistency.

2. Age/Mix of Credit (20%):

The age of your credit accounts and the mix of different types of credit you have are included in this category. Lenders typically like seeing longer borrowing history because it indicates you are a low-risk borrower. So, if your accounts have been open for many years, this will be advantageous for you. Similarly, a mix of different credit types—such as credit cards, mortgages, auto loans, and installment loans—may improve your score. That being said, it is important not to open unnecessary new accounts just to improve this aspect of your score, as this may result in needless debt and increase your risk of missing payments. Opening new lines of credit also increases hard inquiries into your credit history, which I will discuss in factor number 4- “New Credit.”

3. Credit Utilization (20%):

Credit utilization is the ratio of your current credit card balances to your available credit limit. You calculate your credit utilization percentage by dividing your current credit balance by your available credit limit and multiplying by 100. Credit utilization basically communicates how much of your available credit you’re using. High credit utilization (> 30%) can signal to creditors that you’re relying too heavily on credit, meaning you may struggle to pay off any new debt they issue you. Experts typically recommend keeping your credit utilization below 30%. The most ideal scenario would be to keep this ratio below 10%, but I understand this is not always possible.

4. New Credit (11%):

This factor considers how many hard inquiries have been made on your credit file. Hard inquiries occur when a lender investigates your credit file as part of a credit application, as opposed to a soft inquiry, which is unrelated to credit applications and does not affect your credit score. When hard inquiries are executed on your credit file, they typically cause a temporary decrease in your credit score. The logic is that if a person applies for too much new credit in a short period, it may mean that they are taking on more debt than they can handle, which means they are less reliable to repay new debt.

5. Available Credit (2%):

The final and least impactful category considers the total amount of credit available to you. While this makes up a smaller percentage of your score, it still has some effect on your score. The logic behind available credit is that if some other institution(s) believed you were trustworthy with a certain amount of credit, the institution in question should be able to trust you with this amount, too. Since it is based on what other institutions think, as opposed to objective credit files, it is weighted very little.

Business Credit scores

Business credit allows you to access larger amounts of funding for essential business needs such as inventory, long-term assets, and other acquisitions. Lenders typically offer better financing terms for businesses compared to individuals, as businesses are seen to have more potential for growth. Insurance companies also offer more favorable premiums to businesses with better credit scores. In addition to financial benefits, building business credit (instead of relying on personal credit) also helps you separate personal and business records, providing a clearer view of your business health and tax situation. This separation not only simplifies accounting and tax filing but also protects your personal assets from being at risk in case of financial difficulties or a business shutdown.

Establishing business credit is essentially the process of creating a legal business with the local, state, and federal governments, as well as setting up trade or credit accounts with a bank. I will outline the basic steps below- please feel free to check out my article on selecting business forms for more information on types of businesses and EINs.

- Select a Business Form: With regards to business credit, the most advantageous business form is limited liability company (LLC). Since LLCs are separate entities to their owners, they are viewed as being less risky, more scalable, and therefore more attractive to lend to. LLCs can also work in your favor if you have little or poor credit history, since LLCs essentially provide a clean slate to build business credit from. That being said, since you may not have any business operating history or credit, you might still have to put up personal assets as collateral for loans. The less you tie your personal assets to your business debt, the more benefit you will derive from LLCs. Since sole proprietorships and partnerships are closely tied to their owners, you will need to rely on your personal credit history in the early stages of your business if you operate under either of these structures.

- Obtain an EIN

- Obtain a D‑U‑N‑S® Number: While the top three bureaus for personal credit scores are Equifax, Experian, and TransUnion, the only major difference for business credit scores is that Dun & Bradstreet (D&B) replaces TransUnion, with the other two—Equifax and Experian—still tracking business credit. Since Dun & Bradstreet effectively specializes in business credit, I will show you how to obtain a D‑U‑N‑S® number, which potential lenders can use to make an inquiry into your business credit file. First, visit this link. Then, select “Get Started Now” and choose where your business is based, and then complete the application for your D‑U‑N‑S® number.

- Open a Business Bank Account: This will allow you to separate your personal and business bank accounts, which allows you to better track your revenue and expenses. It will also allow you to form a relationship with a bank prior to asking them for credit.

- Open a Trade and/or Credit Account: A trade account is a type of credit account that a business opens with suppliers or vendors. It allows the business to purchase goods or services on credit, usually within a specified period (often 30, 60, or 90 days). This gives you greater flexibility with your cash flow since you do not need to pay upfront for the products or services you need to operate. You can set up a trade account directly with a supplier or vendor, or you can use a third-party service to handle the various aspects of your trade accounts for you. In addition to a trade account, you can also obtain a business credit card from a trusted bank. Some of these credit cards offer cash back rewards, which could help you earn a bit extra on your purchases. However, the same warning for personal credit cards applies to business credit cards, as credit card interest rates are very high.

- Submit Trade References and Make Timely Payments: Submit trade references for vendors or suppliers you have a positive relationship with. Some suppliers and vendors automatically submit trade experiences to D&B, in which case you do not need to manually upload trade references. Making on-time payments is the best way to improve your business credit score and establish good relationships with suppliers and vendors. As your credit score improves, more businesses and lenders will trust you, offering you greater opportunities to build your credit further, creating a positive cycle of growth.

How to Check Your Personal and Business Credit Scores

How to Check Your Personal Credit Score

There are several options for checking your personal credit score.

1. Check for Free Using AnnualCreditReport.com

The Federal Trade Commission (FTC) guarantees that every individual is entitled to one free credit report per year from each of the three major bureaus. You can access these reports online through AnnualCreditReport.com. Each bureau is required to provide a detailed report showing your credit history, including any debts, payment history, and hard inquiries made into your credit file. These reports do not include your actual credit score, but they do allow you an opportunity to check for fraud or errors.

2. Check Your Score for Free via Credit Card or Loan Providers

Many banks and credit card companies offer free access to your FICO® Score or VantageScore® as part of their customer service offerings. For example, CreditWise by Capital One is a tool that lets anyone view their VantageScore® 3.0 for free after entering some personal information (like name, Social Security number, etc.). Financial institutions require personal identifiers like these to access your credit bureau reports and calculate your score. These scores are typically updated monthly, providing a convenient and free way to monitor your credit over time. Also, don’t worry about checking your score too frequently. Since checking your own score is considered a soft inquiry, it will not affect your score.

3. Use Credit Monitoring Services

Credit monitoring services offer access to your credit score, alerts you to any changes in your credit file, and offer practical tips you help you improve your credit score. Some popular credit monitoring services include Credit Karma, Mint, and MyFICO. Some of these services are free, like Credit Karma, while some are paid, like MyFICO. Although paid services often offer a more comprehensive offering, they are generally unnecessary given the extensive information provided by free services.

4. Directly from the Credit Bureaus

You can directly purchase your credit score from the credit bureaus themselves. Equifax offers credit reports for a fee, while Experian and TransUnion offer both free and paid versions. The advantage of this is you are obtaining information directly from the source, but credit reporting through banks and credit monitoring services has become so sophisticated that there remains little advantage for doing so.

When reviewing your credit report, make sure to look for incorrect information (inaccurate account status, outdated debts) and fraudulent activity (accounts opened with your authorization). If you have evidence for either fraudulent activity or incorrect information for a specific bureau, file a direct report with the bureaus through their website.

How to Check Your Business Credit Score

How to Check Your D&B PAYDEX Score

The score reported by Dun & Bradstreet is called a PAYDEX Score, and it ranges from 0-100. The PAYDEX score is based on your payment history with suppliers and lenders. A PAYDEX score of 80 or above is considered good. You can view the various options for retrieving your PAYDEX score here: Grow with D&B Credit Insights – Dun & Bradstreet.

How to Check Your Experian Business Credit Report

Experian offers a Business Credit Report and Intelliscore Plus® score. This score ranges from 1 to 100. Keep up with payments to vendors and monitor your credit regularly to ensure that any negative information is resolved promptly. You can begin the process of checking your Experian business credit report here: Business Credit Report & Scores | Experian.

How to Check Your Equifax Business Credit Report

Equifax provides a Business Credit Report and Business Credit Risk Score. The score ranges from 101 to 992, with higher scores indicating less risk for lenders. Establish credit with vendors who report to Equifax, and ensure you keep up with payments. View your Equifax report here: Commercial | Business | Equifax.

How to Use Credit Monitoring Services

Similar to personal credit monitoring services, business credit monitoring services, the most popular of which is Nav, allow you to access business credit scores for free. Nav offers a free plan that shows business credit scores from Dun & Bradstreet, Experian, and Equifax. An added benefit of Nav is it can track your personal credit score, too, so it is convenient for small business owners with personal and business credit scores. You can explore their product offerings at Business credit building │ Nav.

You might also purchase your business credit score and report directly from the credit bureaus or other third-party services. As with personal credit scores, this may prove unnecessary given the vast range of free tools available to small business owners.

-> Remember, business credit scores measure the credit worthiness of your business (assuming it is a separate entity) and personal credit scores measure the credit worthiness of you as an individual. Regardless, excellent credit scores do not happen overnight. Making on-time payments and financially responsible decisions over an extended period of time is the key to achieving great credit scores.

Leave a comment